Even though Fed Chair Jerome Powell remarked that it’s too soon to definitively conclude that rate hikes are finished, the financial markets have, in fact, decided they’re finished. As of December 4, 2023, interest-rate futures traders (the people who make a lot of money being right about where rates will go) expect the Fed to cut the federal funds rate, which currently falls between 5.25% and 5.50%, by 1.25%.

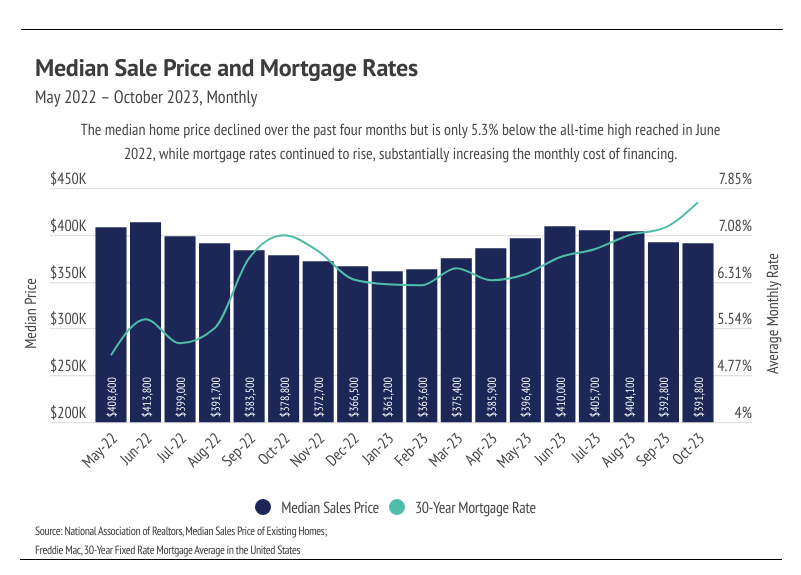

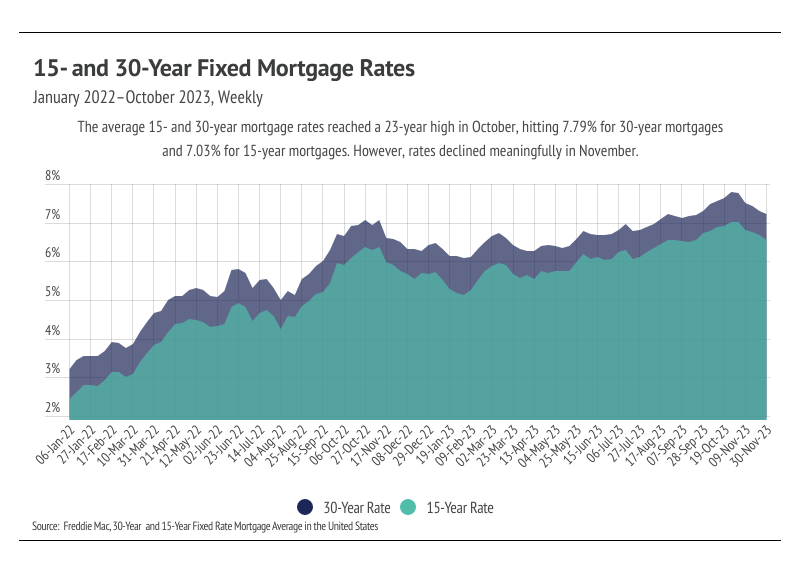

As a quick recap, the Fed dropped the fed funds rate effectively to 0% at the start of the pandemic and purchased mortgage-backed securities. The already historically low average 30-year mortgage rate then fell even further, reaching a record low of 2.65% in early 2021, which fueled the housing boom from June 2020 to June 2022. Inflation spiked in 2021, hitting levels not seen since the early 1980s and causing the Fed to begin rate hikes in March 2022, which trickled through markets quickly. From the beginning to the end of 2022, mortgage rates more than doubled, ending the white hot housing market and creating the slow-paced 2023 market. Mortgage rates continued to rise in 2023, hitting a 23-year high of 7.79% in October. Luckily, the average 30-year mortgage rate contracted in November 2023, falling to 7.22% by the end of the month.

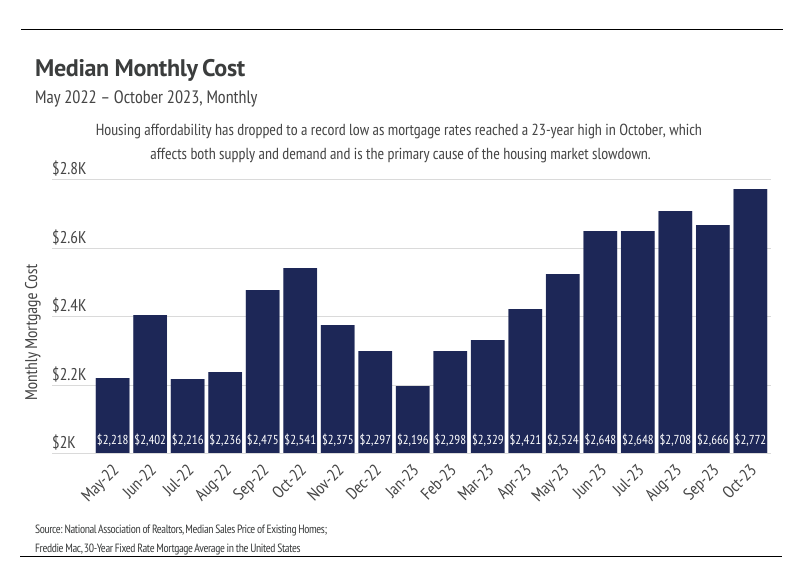

It’s hard to convey the full significance of higher mortgage rates on the housing market but, in short, they are the primary driver of the market slowdown. This is evidenced by the fact that the market began slowing down at almost the exact same time that the Fed began their rate hikes. In October 2023, a buyer’s monthly cost reached an all-time high when accounting for the cost of financing a mortgage. Redfin reported the highest rate of buyers backing out of home purchases on record, as home buyers experienced the sticker shock of the cost to finance the home. It should come as no surprise that sales continued to fall and will likely continue to decline through the winter months.

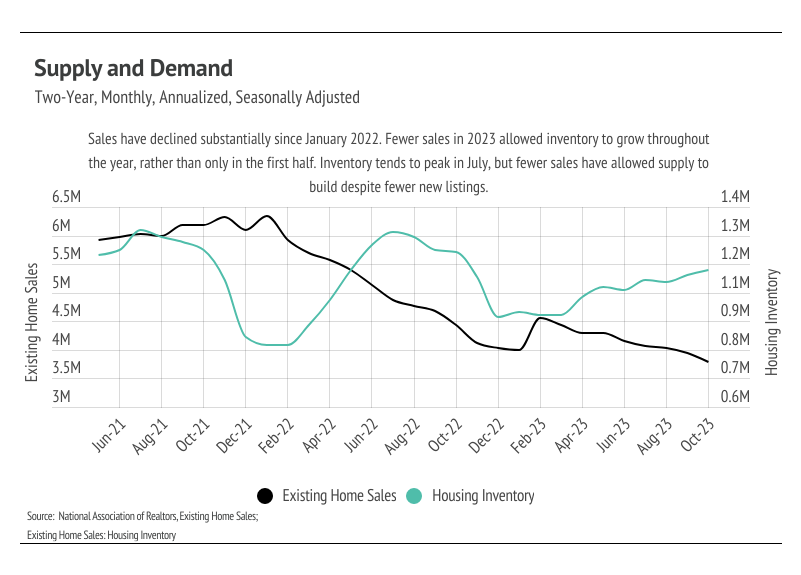

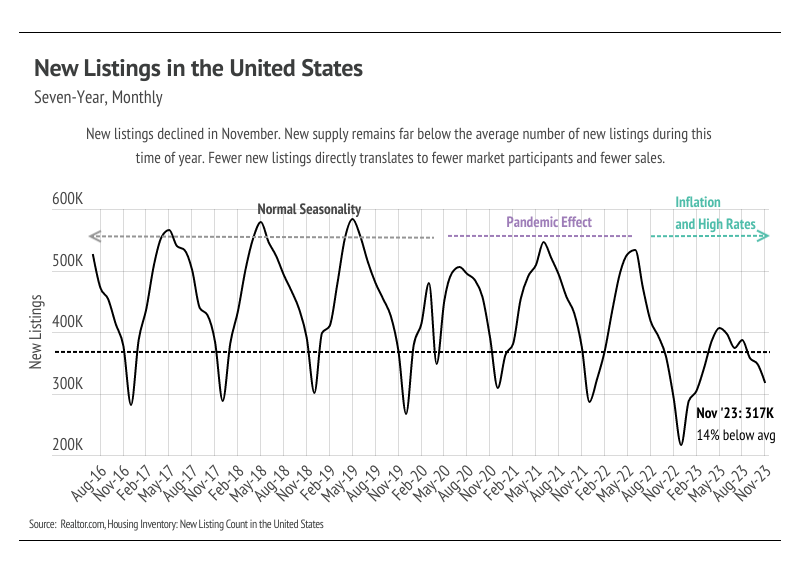

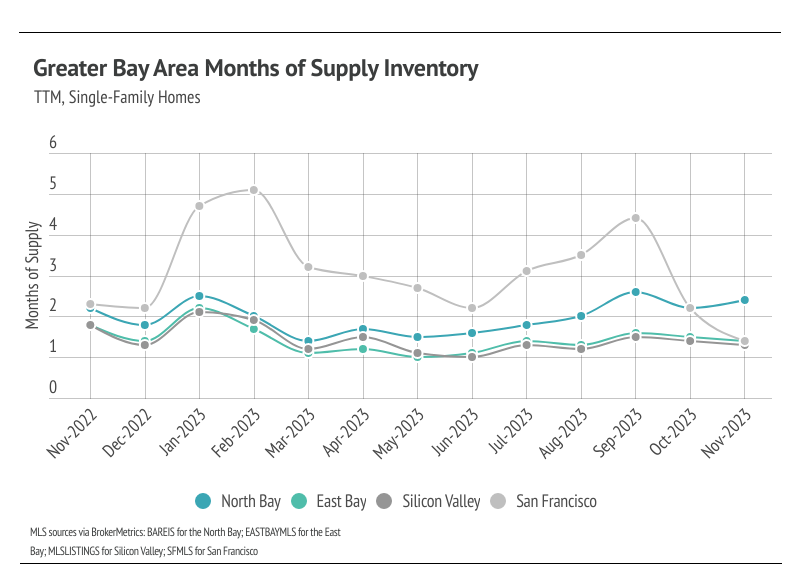

Now, back to our outlook for the year ahead. The falling sales in 2023 have allowed inventory to grow, which is much needed. Although inventory is still down 6% year over year, it has increased 20% in 2023 and will likely continue to increase through the rest of the year, which is far different from the typical seasonal trend of increasing in the first half of the year and declining in the second. In Q1 2024, we expect inventory to rise further, helping ease the low supply problem. Greater supply will be necessary because mortgage rates should decrease meaningfully with the anticipated rate cuts, driving up demand. A 1% decrease in interest rate equates to a 10% decrease in monthly financing costs. At this point, we expect a large number of would-be buyers to wait a little longer to gain more clarity around rate cuts in 2024 and hit the market in the spring and summer months.

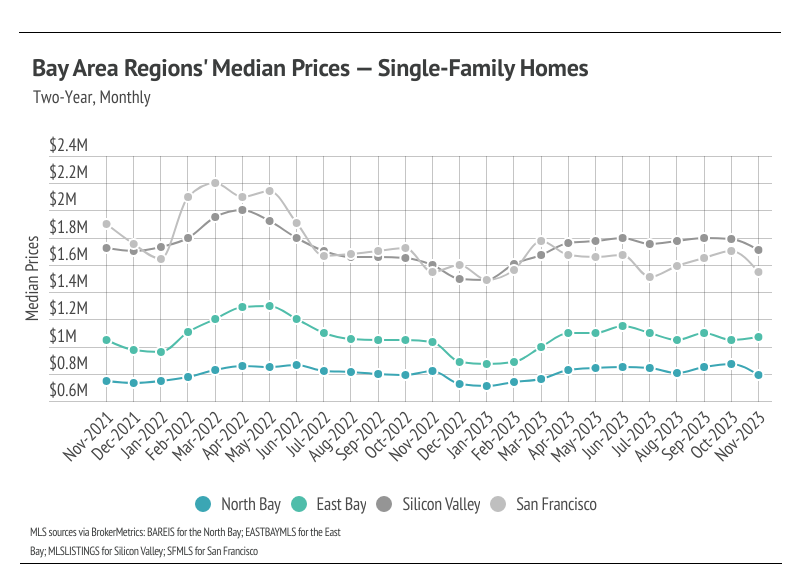

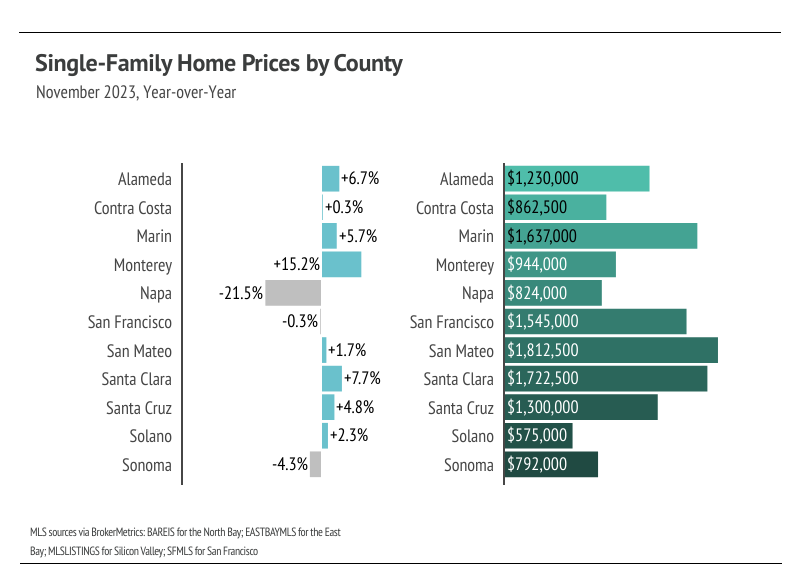

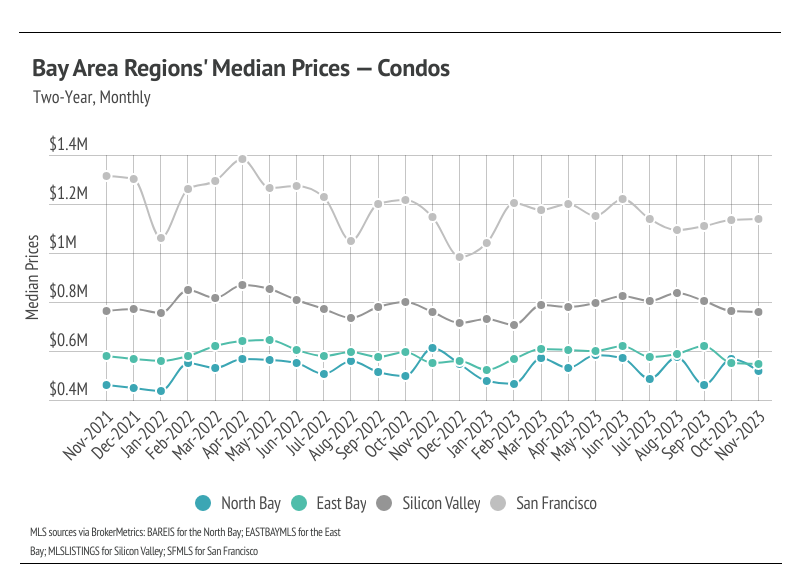

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. In general, higher-priced regions (the West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (the South and Midwest) because of the absolute dollar cost of the rate hikes and limited ability to build new homes. The National Association of Realtors’ Chief Economist Lawrence Yun recently remarked that multiple offers are still occurring, especially on starter and mid-priced homes, even as price concessions are happening in the upper end of the market. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home. |

|

|

Upgrade Your Home With These 2024 Design Trends

Upgrade Your Home With These 2024 Design Trends