If you’re an avid reader of our newsletters, you may recall discussions of a possible recession a few months ago. We, of course, weren’t the only ones talking about it, but it was a little early to opine. We’re happy to say that a recession likely isn’t on the horizon but that there is one major caveat: the debt ceiling. Before we discuss the debt ceiling, we’ll cover the economic indicators that brought us to the conclusion that we’re entering a period of slower economic growth rather than a recession.

Recessions used to be defined by a fall in Gross Domestic Product (GDP) for two consecutive quarters. For what it’s worth, Real GDP in the fourth quarter of 2022 was up 1% year-over-year and 0.7% quarter-over-quarter. However, the National Bureau of Economic Research (NBER) takes a more nuanced approach by considering nonfarm payrolls, industrial production, and retail sales, among other indicators. The U.S. employment rate is still strong despite some notable high-profile companies, especially in tech, announcing mass layoffs. The unemployment rate is 3.5%, which is about as low as we’ve seen in modern history. Additionally, initial unemployment claims and continued claims have been at pre-pandemic levels for about 13 months and 11 months, respectively. Total Nonfarm Private Payroll Employment data (seasonally adjusted) from ADP shows that job growth stagnated in the second half of 2022 but didn’t decline. With over 10 million job openings in the country, the level of unemployment should remain historically low for the foreseeable future. As a general rule, a high employment rate is good for both the housing market and the overall economy for fairly straightforward reasons: Employed people make money, so they can pay their bills and not default on their debt.

Inflation is still far above the Fed’s 2% target, but it is coming down. December 2020 was the last month of the steady ~2% year-over-year inflation rate we’d seen over the past decade. Inflation rose rapidly in 2021 and the first half of 2022. Early signs show we are entering a period of disinflation — a temporary slowing of the pace of price inflation — not deflation, which is a general drop in price level. Said differently, goods and services will get more expensive at a slower rate than we’ve seen over the past two years, which, we suppose, is better than nothing.

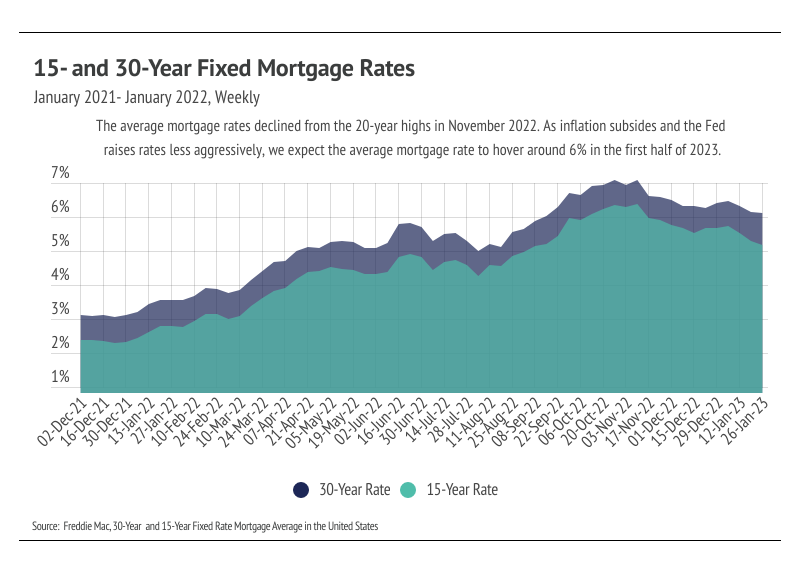

We expect mortgage rates to hover around 6% for the first half of 2023, unless the world’s faith in the United States’ ability to pay its debt obligation further erodes because of Congress’ continued delays in raising the debt ceiling. Mortgage rates are typically about 1.8% higher than 10-year U.S. Treasury bond yields, so a spike in 10-year Treasury yields also spikes mortgage rates. The current Congress certainly seems to be the most amenable to default. However, the likelihood of that happening is low, considering that the politics of a self-inflicted U.S. and global recession not seen since the Great Depression would be, objectively, outside of anyone’s best interests. Were it to happen, though, we would likely see mortgage rates easily near 8% and wealth substantially decrease, pricing a significant number of potential buyers out of the housing market.

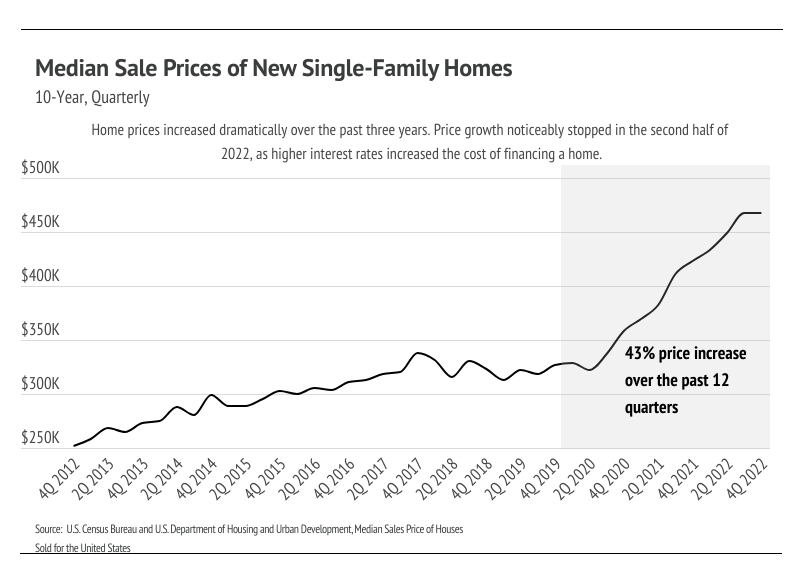

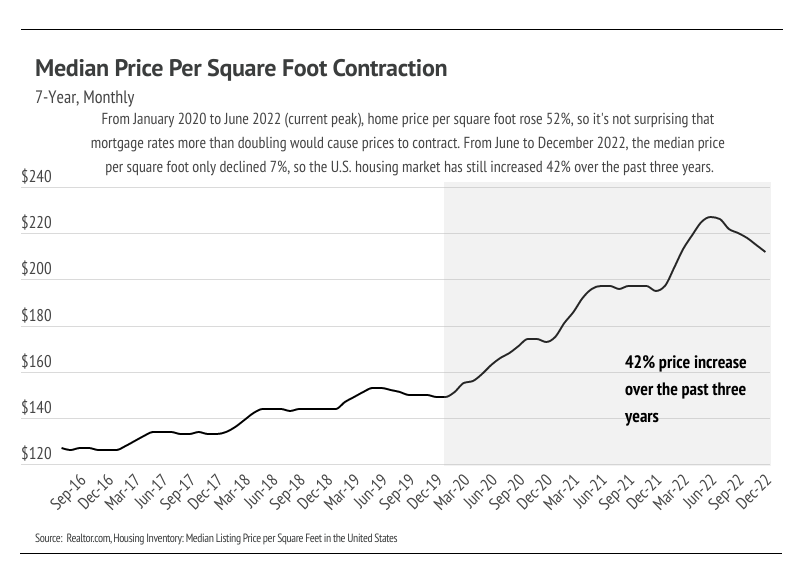

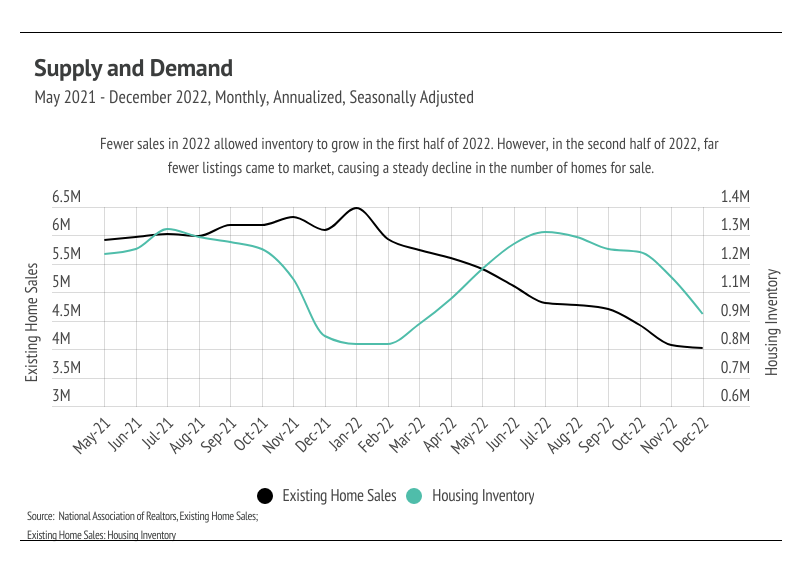

We expect this year to be marked by fewer buyers and sellers, making the market more balanced. On average, sellers can expect fewer offers and far fewer offers above list price than we saw in 2021 and the first half of 2022. Buyers may need more time to find the right home for them as fewer new listings come to market. Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage of your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home. |

|

|

Stress-Free Home Cleaning: 27 Practical Tactics for Busy Households

Stress-Free Home Cleaning: 27 Practical Tactics for Busy Households