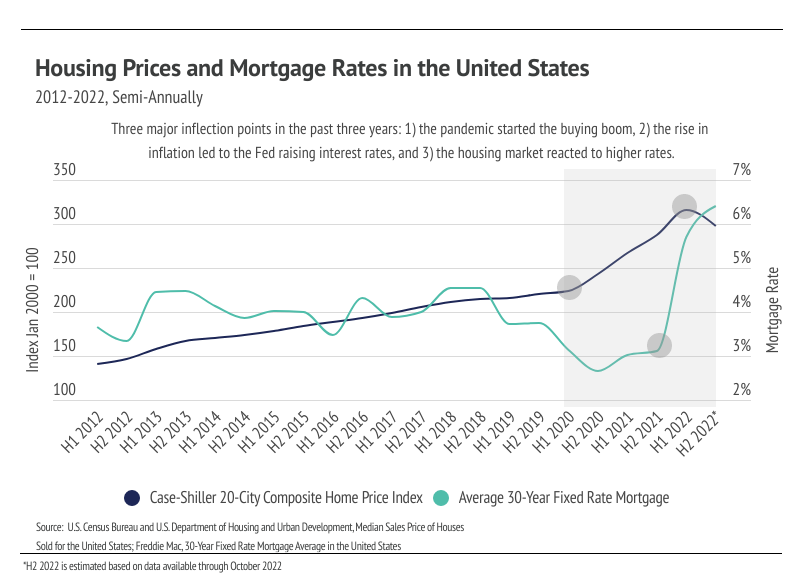

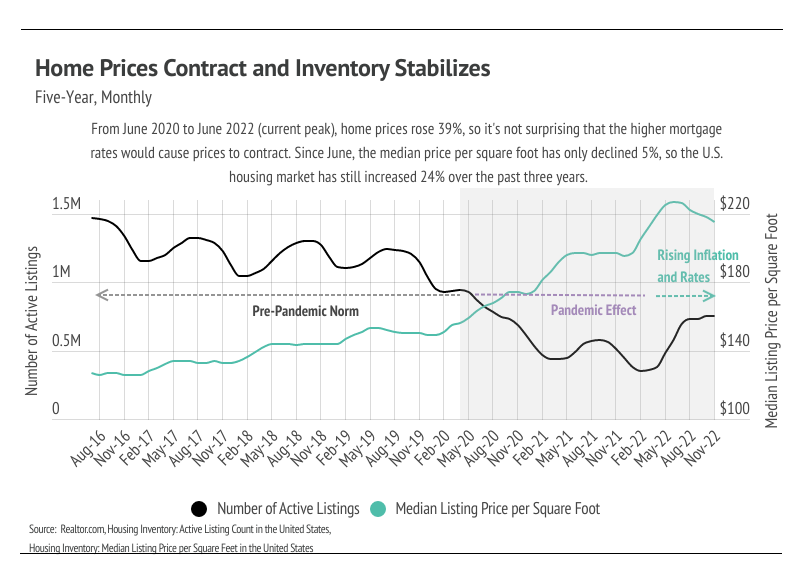

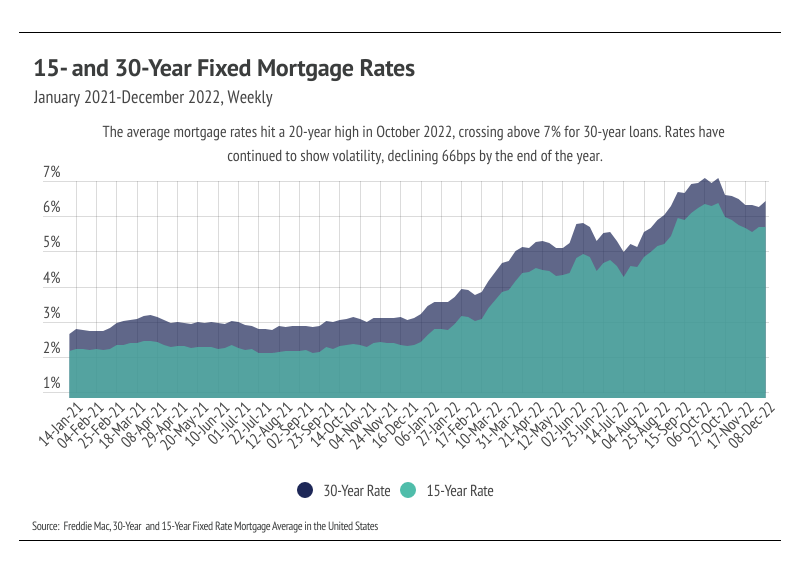

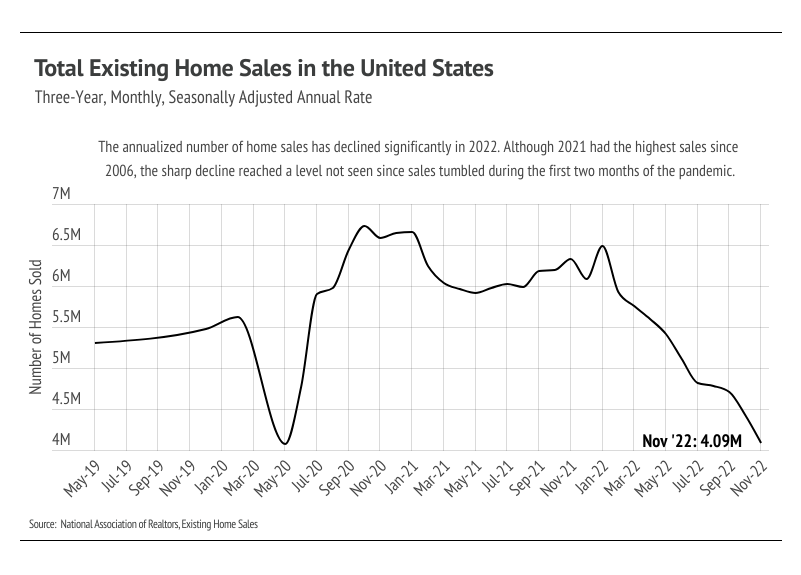

Major U.S. Housing Events 2020 - 2022 Mid-March 2020 - May 2020: Concern over COVID-19 skyrocketed, leading to shelter-in-place orders across the United States and around the world. Seemingly everything shut down — including the real estate market because it’s very hard to buy or sell a home when you aren’t supposed to gather. By about the end of May 2020, it became clear that the virus wasn’t going away quickly, triggering the housing boom and the start of ultra-low mortgage rates. June 2020 - December 2020: Asset prices, from housing to stocks to crypto to art, exploded due to a combination of easy money and a change in consumer behavior. The Federal Reserve lowered interest rates and poured money into the market, increasing the amount of money in circulation by 17% from February 2020 to May 2020. By the end of 2020, the money supply increased 24%, and by the end of 2021, it had risen 40%. Buyers were priced into the market as mortgage rates declined under 3% for the first time ever. Without a clear end to the pandemic in sight, buyers were incentivized to find a home they wanted to spend a lot of time in not only for rest, but also to work. With the increase in buyers, demand outstripped supply like we’ve never seen before. The number of homes for sale in the United States declined 34% in six months, while overall home prices increased 9%, according to the S&P/Case-Shiller 20-City Composite Home Price Index. January 2021 - December 2021: The year opened with the lowest 30-year average fixed mortgage rate on record: 2.65%. Mortgage rates hovered around 3% the entire year, with an average mortgage rate of 2.96% in 2021. The increase in buyers in the second half of 2020 was only a preview for 2021 sales, which were the highest since 2006. By the end of the year, home prices increased another 17% (29% in total since May 2020), and the number of homes for sale fell 52% since May 2020. Additionally, inflation rose quickly, and we closed the year with inflation at 7.09%, a level not seen since 1982. The Fed had one main tool to combat inflation: raising interest rates. Because the Fed said in December that it would begin raising rates in March 2022, it created the final buying boom as buyers and sellers rushed to the market to lock in low rates. January 2022 - June 2022: The last true sales spike occurred during the first quarter of 2022, which drove home prices up 5%. Sales began to slow, as did price growth. Home prices reached an all-time high in June 2022, increasing 42% since June 2020, which was the sharpest and quickest rise in home prices ever recorded. By the end of June, mortgage rates had risen 2.6% in 2022, which drastically decreased affordability. July 2022 - December 2022: During the second half of 2022, the housing market cooled significantly. Demand softened for several key reasons: higher interest rates, a return to seasonal market trends where prices increase in the first half of the year and decrease slightly in the second, and mean-reversion (about a million homes were sold above the average in 2021, and about a million fewer than the average were sold in 2022). We closed the year with high and volatile mortgage rates, hitting 20-year highs in October and November. The fourth quarter gives us a decent picture of what’s ahead.

|

|

|

My Home Didn’t Sell! Now What?

My Home Didn’t Sell! Now What?